Since the Canadian regulatory shift in 2022, pass-the-fee payments has emerged as a strategy that enables companies to maintain competitive pricing while addressing the high costs of payment processing. This approach offers a transparent way to offset credit card processing fees, ensuring that customers who pay with cash or debit aren’t inadvertently subsidizing those who use credit cards. By adopting pass-the-fee, companies can allocate costs fairly, preserving the integrity of pricing for all consumers.

Though it may seem like a small change, this system fosters transparency, allowing customers to clearly understand what they’re paying for. It also helps businesses keep operational costs in check while promoting fairness for everyone, regardless of payment method. In this article, we’ll explore how pass-the-fee can benefit both businesses and consumers, providing a strategic advantage in today’s market.

Why Businesses Choose Pass-the-Fee

For many, implementing Pass-the-Fee is a smart move to manage credit card processing costs without compromising their pricing. According to the Financial Consumer Agency of Canada, these fees can range from 1.5% to 3.5% of the transaction. For emerging businesses or businesses with thin margins, these fees can quickly eat into their earnings.

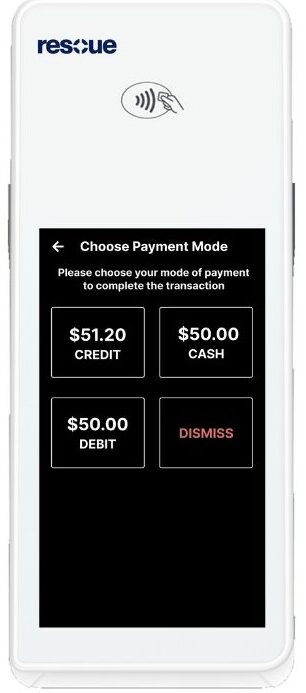

Rather than absorbing these costs or increasing prices for all customers, you can pass the fees onto credit card users – so, customers who choose to use credit cards pay a small surcharge, while those paying with cash or debit are unaffected by the extra fees.

This practice helps merchants keep prices stable across the board, allowing them to stay competitive while ensuring that they are covering the costs incurred when accepting credit card payments.

The Costs of Credit Card Processing

To fully understand passing the fee, we must first look at the real costs businesses face when accepting credit card payments.

Credit card transactions come with several fees that add up quickly. These include:

- Interchange Fees: Fees paid to the credit card networks (Visa, Mastercard, etc.)

- Assessment Fees: Charged by the card networks for using their platforms.

- Processor Fees: Paid to the payment processor who facilitates the transaction.

These fees can range from 1.5% to 3.5% of the transaction amount, depending on factors such as the type of card used, how it was accepted, and more.

For businesses, these can make it challenging to stay profitable. Without a pass-the-fee program, merchants have to absorb these costs (cutting into their margins) or raise prices for all customers – burdening those who pay with cash or debit.

How Pass-the-Fee Leads to Fair Pricing

While a surcharge offsets processing fees, it also helps create a fairer pricing structure for all involved:

- Aligning Costs with Usage: By passing the fee on credit card transactions, businesses ensure that those who enjoy the benefits of credit card rewards (like air miles or cash-back) pay for the convenience of using their card.

- No Hidden Cross-Subsidization: Without this, businesses often raise prices across the board to account for credit card processing fees. This means that cash and debit users, who don’t incur these fees, end up subsidizing the costs of credit cards. By passing the fee directly to credit card users, businesses eliminate this hidden cost-sharing.

- A Win for Budget-Conscious Customers: For customers who prefer using cash or debit, this ensures they aren’t paying higher prices than necessary. It’s a fairer model that ensures that fees align with consumers’ preferred payment method.

Real-World Canadian Examples of Pass-the-Fee

- Professional Services: Law offices, accounting firms, and other service-based businesses are applying surcharges to offset high processing fees for larger invoices. Often providing fee-free options such as wire transfers or cheques as offramps.

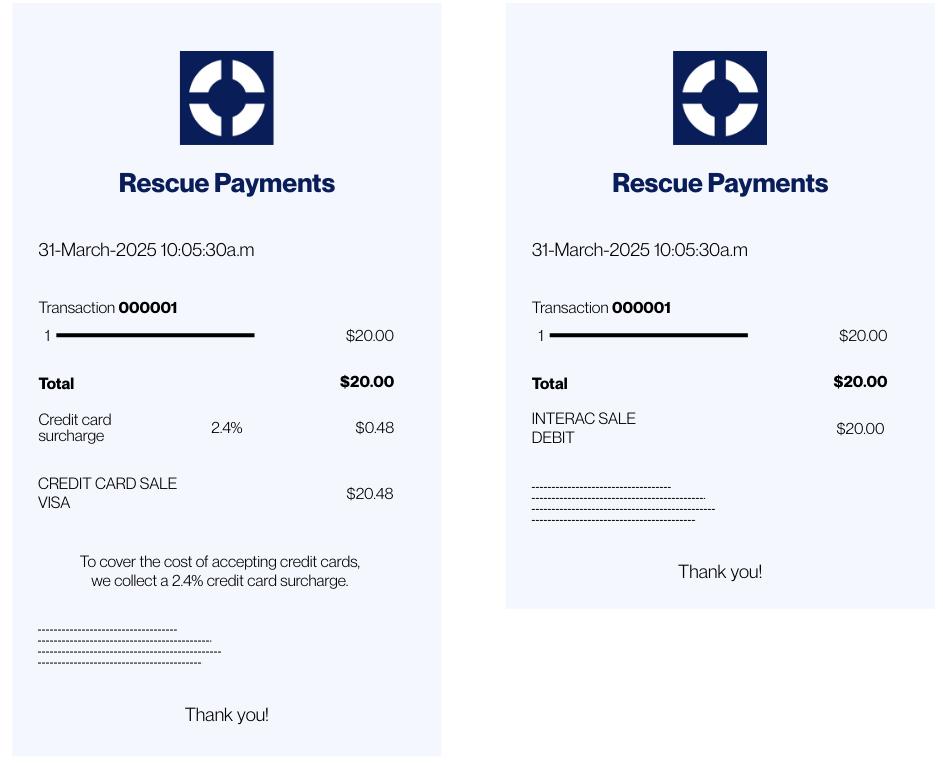

- Restaurants: In Toronto and Vancouver, many restaurants have introduced pass-the-fee programs, adding a 2.4% surcharge on credit card transactions – allowing them to keep menu prices stable.

- Service-Based Businesses: Mechanics, barbershops, and salons across Canada have begun implementing pass-the-fee, helping them cover credit card fees without raising their service rates for customers paying with non-credit methods.

- Medical Clinics: Dental and medical clinics are increasingly passing on credit card processing fees to patients, particularly for elective treatments or larger invoices. This allows clinics to keep pricing consistency while offering fee-free options and maintaining margins.

- SaaS Platforms: To address rising credit card fees, many SaaS platforms are adopting surcharges for high-value contracts or subscriptions. Some apply surcharges to credit card payments, while others offer clients a discount for paying via more cost-effective methods, like wire transfers or debit.

By adopting this model, businesses ensure they can stay competitive and continue offering fair pricing.

Pass-the-Fee in Quebec: Implementing a Dual Pricing Model

In Quebec, Pass-the-Fee programs are prohibited due to consumer protection laws. However, businesses can still implement a dual pricing model to offer an alternative solution.

Under this model, businesses can charge different prices depending on the payment method. Customers paying with credit cards will see a higher price, while those using debit or cash will benefit from the lower price.

For Quebec-based businesses looking to implement this, Rescue Payments offers guidance and support. We specialize in helping businesses navigate the complexities of payment processing and compliance with local regulations. Our resources can help businesses create transparent pricing models that both comply with the law and benefit customers.

The Impact on Customer Perception

Surcharging brings clarity to pricing and helps build consumer trust. When businesses clearly disclose that they are applying a surcharge, customers are more likely to accept it as a natural part of doing business.

By linking the surcharge directly to the cost of credit card processing, businesses show that they aren’t inflating base prices to cover fees. This level of transparency strengthens customer relationships and fosters loyalty.

Surcharging also allows consumers to make informed decisions about their payment methods. Those who use credit cards can weigh the benefits of rewards against the additional cost of the surcharge, while others may opt for debit or cash to avoid the fee altogether.

Legal Considerations: Navigating the Pass-the-Fee Landscape in Canada

Here’s what businesses need to know for surcharging in Canada:

Provincial and Territorial Regulations: In most provinces and territories, businesses can apply surcharges as long as they are clearly disclosed to customers before the transaction (apart from Quebec).

Compliance Tips: To implement pass-the-fee practices fairly and legally, businesses should:

- Disclose surcharges before the transaction.

- Follow the 2.4% cap for credit card processing costs.

- Offer alternative, fee-free payment methods like cash and debit.

- Stay updated on provincial and territorial regulations.

The Canadian Federation of Independent Business (CFIB) provides resources to help businesses navigate these legal considerations. At Rescue Payments, we provide expert advice to help businesses implement these solutions in compliance with the law. We also help you stay updated on any changes in provincial and territorial regulations to ensure ongoing compliance.

A Fairer Future with Pass-the-Fee

Pass-the-Fee programs offer more than just a way to cover credit card processing fees—they represent a shift towards transparency in Canadian pricing. For businesses, these programs provide a manageable way to handle high processing fees without increasing prices for customers who pay with debit or cash. For consumers, Pass-the-Fee gives them the freedom to choose the most cost-effective payment method without hidden fees embedded in product prices.

As surcharges continue to become more common across Canada, they create a more equitable environment for both merchants and customers. For businesses looking for further guidance on navigating credit card surcharges, here are 81 most common questions Canadian merchants and small business owners may have.

Rescue Payments is here to help Canadian businesses understand and implement this—ensuring that pricing remains consistent, fair, and legally compliant across all regions.